Tuttle Law Offices

March 11, 2016 |

Identification, assessment and collection of Antidumping and Countervailing Duties (AD/CVD) continues to be a high enforcement priority for U.S. Customs and Border Protection (“CBP”). CBP reports that in FY 2015:

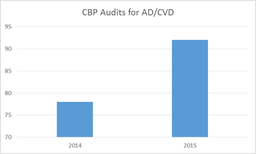

In addition, CBP conducted 92 audits of importers of AD/CVD commodities and identified $69 million in AD/CVD loss of revenue with $7 million collected to date. CBP also levied 18 monetary penalties totaling over $60 million on importers for fraud, gross negligence and negligence for AD/CVD violations under 19 U.S.C. § 1592 (including the assessment of $45.5 million in penalties for AD/CVD violations on importers of steel products). CBP also carried out 28,783 entry summary reviews on potential AD/CVD violations and identified over $29 million in AD/CVD loss of revenue. The top AD/CVD violations identified were for tires, solar cells and pencils. In comparison, in FY 2014 CBP collected $508.5 million in AD/CVD cash deposits, conducted 78 audits of importers of AD/CVD commodities, and identified $24.6 million AD/CVD discrepancies and collected $8.5 million.

Commodities involved in the audits include aluminum extrusions, bearings, candles, nails, lock washers, pencils, plastic bags, ribbons, shrimp, solar cells, steel pipe, tires, tissue paper, wooden bedroom furniture and wood flooring. These statistics show not only CBP’s ongoing enforcement efforts, but that importers have a lot of work to do to increase their understanding of the AD/CVD process and how they can take steps to improve their compliance efforts to identify and properly report goods that are subject to AD/CVD duties. Apart from outright fraud in the avoidance of payment of AD/CVD duties, importers frequently fail to identify goods at the time of importation as being subject to AD/CVD duties. This can occur for a multiple of reasons, including:

Importers can improve their compliance rate with AD/CVD duties and avoid potential penalties and back payments by implementing internal controls that focus on compliance with AD/CVD orders. Internal controls for compliance with AD/CVD orders include:

While AD/CVD orders include the Harmonized Tariff Schedule (HTS) classification for goods subject to the scope of the order and investigation, this information is only provided for convenience and customs purposes. The written description of the scope is dispositive. Importers can identify products currently subject to AD/CVD Orders by checking various websites, including a listing by the Department of Commerce of Products currently subject to AD/CVD Orders, the U.S. International Trade Commission (ITC) webpage on Antidumping and Countervailing Duty Investigations and the CBP Automated Commercial Environment (ACE) report ES-105 ADCVD Active Case List (https://ace.cbp.dhs.gov/). Importers can also take a number of steps to reduce potential AD/CVD liabilities by increasing their engagement in the AD/CVD process. This includes:

While the annual administrative review is used to calculate assessment rates and new cash deposit rates based on a period of sales subsequent to the investigation, a CCR addresses questions about the applicability of the order. For example, “no interest revocations,” where partial or total revocation of the order is warranted because domestic parties are no longer interested in covering certain products. CCRs may also address the applicability of cash deposit and assessment rates after there have been changes in the structure of a respondent, such as a merger or “successor-in-interest,” or “successorship,” determinations. If you have questions about this or other international trade matters, please contact George Tuttle, III, at geo@tuttlelaw.com or at (415) 986-8780. Cindy DeLeon, Senior Trade Auditor, with Deleon Trade, contributed to the writing of this article. For further information about Ms. DeLeon and Deleon Trade, you can visit Deleon-Trade.com. Thank you, Cindy. George R. Tuttle, III, is an attorney with the Law Offices of George R. Tuttle in the San Francisco Bay Area.

The information in this article is general in nature, and is not intended to constitute legal advice or to create an attorney-client relationship with respect to any event or occurrence, and may not be considered as such. Copyright © 2016 by Tuttle Law Offices.All rights reserved. Information has been obtained from sources believed to be reliable. However, because of the possibility of human or mechanical error by our offices or by others, we do not guarantee the accuracy, adequacy, or completeness of any information and are not responsible for any errors, omissions, or for the results obtained from the use of such information.

|